Healthcare Investment Trends in Asia 2026: Key Trends PE Firms Should Watch

For Clients

For healthcare private equity investors, the core question is shifting. It is no longer simply “which markets will grow fastest,” but rather: which healthcare systems can reliably convert demand into scalable, investable returns under real operating constraints. The way investors answer that question shapes the healthcare industry trends across Asia in 2026.

While the United States still accounts for the majority of healthcare private equity activity, investors are increasingly looking abroad for growth. Asia’s healthcare market is projected to exceed $5 trillion by 2030, driven by aging populations, rising healthcare spending, and the rapid adoption of digital health. Yet the opportunity is not evenly distributed. Success often depends less on identifying attractive markets and more on understanding local operating realities.

For investors evaluating Asia, the competitive advantage increasingly comes from combining market data with local expertise.

The Healthcare Industry Trends Driving Asia’s $5 Trillion Opportunity

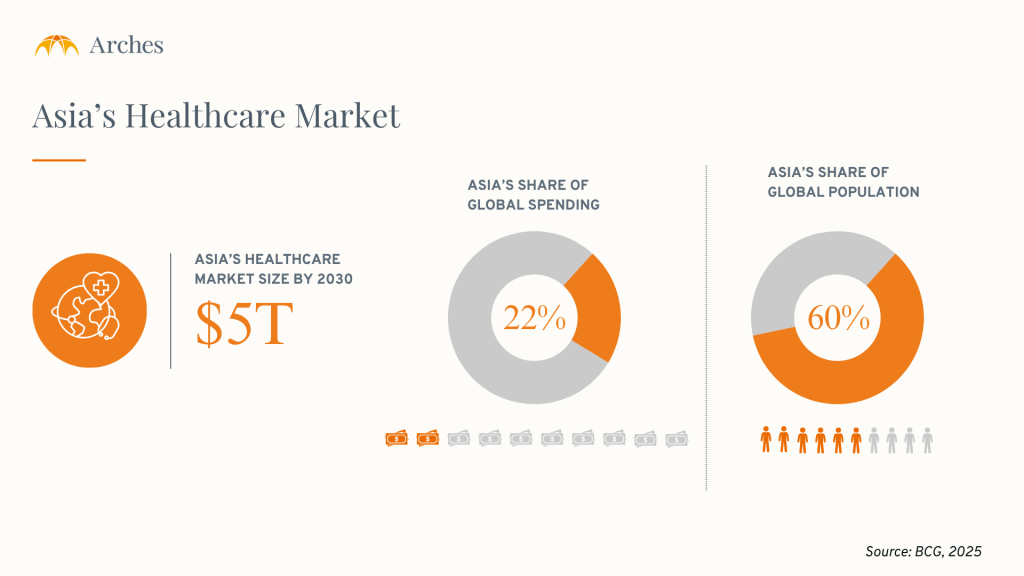

Asia’s healthcare market is on track to reach roughly $5 trillion by 2030 and to drive about 40% of global sector growth. But the region still accounts for just 22% of global healthcare spending, even while holding 60% of the world’s population (BCG, 2025). That gap between need and spend is the engine of the whole thesis: demand is rising while supply stays under-built.

Southeast Asia shows the shortfall most clearly, and the structural reasons private capital is filling it:

- New health-infrastructure spending is estimated at up to US$39.1 billion per year through 2030, with Indonesia alone accounting for about 40% of that need (Australian Government DFAT, 2024).

- Most Southeast Asian governments allocate under 4% of GDP to healthcare, against roughly 9% across OECD countries.

- Around 70% of hospital beds across Asia are already privately funded (Fortune, 2026).

Private capital is now moving to fill exactly this shortfall. The drivers differ sharply by market, and so does the path to returns. Identifying the dominant trend in each geography is the core analytical task.

How Capital Is Shifting Along the Newest Healthcare Industry Trends

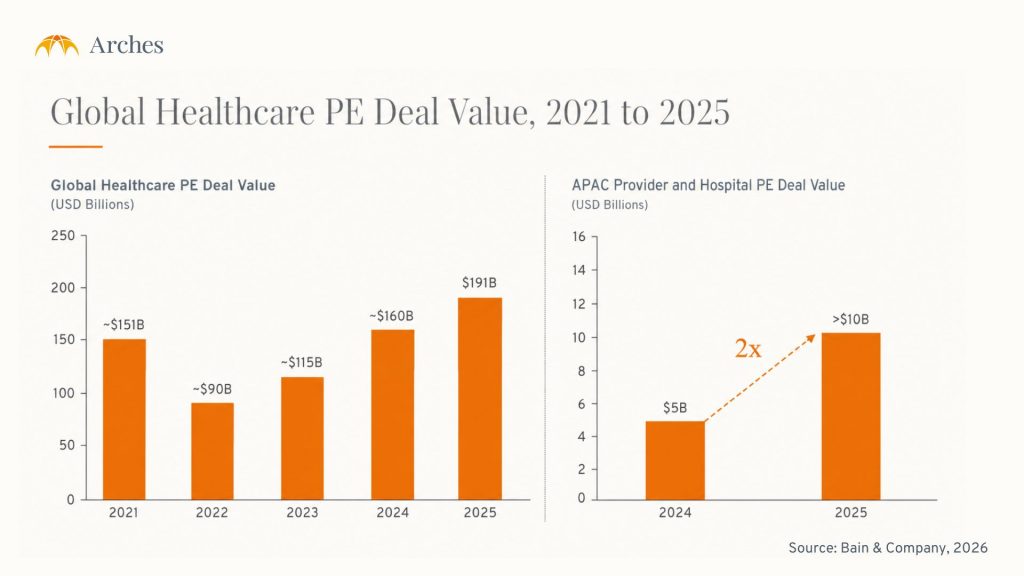

Global healthcare private equity hit a record in 2025: an estimated $191 billion across 445 buyouts. Asia-Pacific set its own record too, beating its 2021 high by more than 30% (Bain & Company, 2026).

For PE investors, the total matters less than the direction. The real question is where the capital is going. Three themes now define healthcare industry trends across the region:

- Digital health and AI, moving from a growth story to operating infrastructure.

- Specialty care platforms, offering focused models with stronger unit economics.

- Aging and eldercare are opening an entirely new investment category.

Digital Health and AI: From Growth Story to Infrastructure

Healthcare systems across Asia face the same squeeze: too few clinicians, rising chronic disease, and large underserved rural populations. Technology that scales care has moved from a “nice to have” to a structural necessity.

The market reflects it. Global AI-in-healthcare is projected to grow from $21.66 billion in 2025 to $110.61 billion by 2030, a 38.6% CAGR, with Asia-Pacific the fastest-growing region (MarketsandMarkets, 2025). India alone is forecast to jump from $1.6 billion in 2025 to $18.6 billion by 2035, led by diagnostics (Medical Buyer, 2026).

For PE investors, AI works as a margin-expansion lever inside operating assets, reshaping value creation by asset type:

- Hospitals: throughput optimization.

- Diagnostics: lower cost per test.

- Clinics: workflow automation and capacity expansion.

The implication for PE is concrete: AI now belongs inside the operating-model thesis itself, underwritten to drive growth and margin rather than treated as a side technology bet (Bain & Company, 2026).

Specialty Care Platforms: Focused Models, Stronger Economics

Investors are moving from broad hospital platforms toward focused specialty providers with recurring demand and clearer expansion paths. Single-specialty formats scale faster, deliver higher returns on capital, and replicate well across underserved geographies.

The active verticals are familiar:

- Oncology and cardiology, tracking chronic-disease burden.

- Fertility and mother-and-child care, with high turnover and brand loyalty.

- Nephrology and ophthalmology are both suited to roll-ups.

India shows the model maturing. Single-specialty hospitals are projected to grow from roughly $15 billion to $31 billion within three to four years, and more than 40% of PE healthcare investment since 2019 has gone to single-specialty players, up from just over 15% in 2015 to 2018 (Asia Healthcare Holdings / Avendus, 2025). Appetite is intense: in 2025, KKR, TPG, Warburg Pincus, Advent, CVC, Permira, and Kedaara competed for a 25% stake in maternity chain Cloudnine at around 10,000 crore rupees (Outlook Business, 2025).

For PE investors, specialty care reads as a repeatable platform model offering:

- Predictable EBITDA expansion through standardization,

- Geographic roll-up potential,

- Stronger exit visibility than general hospitals.

The binding constraint is execution. Operator quality and local physician alignment vary sharply by market, and that is where most underwriting risk sits.

Aging and Eldercare: A New Investment Category

Japan, South Korea, and increasingly China are aging faster than almost any societies in history, creating demand for a new layer of infrastructure around older populations.

China shows the scale. Its 60-plus population hit 297 million (21.1%) in 2023, and the country turns “super-aged” around 2030. The silver economy has followed:

- About 8.3 trillion yuan ($1.16 trillion) in 2024, projected to reach 25 trillion yuan by 2030 (China Center for Information Industry Development, 2025);

- Senior care alone is estimated to be above 22 trillion yuan by the early 2030s (Ping An Group, 2023).

For PE investors, this opens adjacent categories such as assisted living, home care, rehabilitation devices, chronic-disease management, and age-tech. These are long-duration assets with demand locked in for decades, the exact profile patient capital is built to underwrite.

Where Investors Are Looking in 2026: A Market-by-Market View

The three themes do not appear uniformly. Each major market expresses a different combination, which is why a regional thesis has to be built market by market.

China: Healthcare AI and the Silver Economy

China is where the digital-health and eldercare themes converge most powerfully.

- After a multi-year slowdown, healthcare PE in Greater China more than doubled both its 2024 volume and value in 2025, led by biopharma and medtech, though still below historical highs (Bain & Company, 2026).

- A vast aging population, an expanding silver economy, and government backing for AI-enabled care make it a high-ceiling but timing-sensitive market that rewards local execution.

Japan: Aging Creates Durable, Long-Term Demand

Japan has the world’s oldest population: roughly 30% are already aged 65 or older, heading toward one-third by 2050 (Statista / UN World Population Prospects, 2025). For investors, it offers lower-volatility, long-horizon exposure to the aging thesis:

- Deep, stable demand for eldercare, chronic-disease management, and efficiency technology;

- Active dealmaking in 2025, often through large carve-outs (Bain & Company, 2026).

Indonesia: The Private Healthcare Expansion Play

Indonesia is the clearest capacity-expansion play, with demand outrunning supply on two fronts:

- It accounts for roughly 40% of Southeast Asia’s $39.1 billion annual health-infrastructure need (Australian Government DFAT, 2024);

- Its JKN insurance scheme now covers more than 95% of the population, expanding access faster than beds and facilities can keep up (P4H Network, 2025).

That mismatch is drawing regional capital; Singapore-based Quadria Capital, for example, holds Indonesia’s Hermina Hospitals (Fortune, 2026). For investors, it is a volume-and-build story underpinned by structural undersupply.

South Korea: From Manufacturing Powerhouse to Healthcare Innovation Hub

South Korea is shifting from contract manufacturing toward genuine healthcare innovation, while carrying the same demographic tailwind as its neighbors.

- It now ranks third worldwide in new drug discoveries, with more than 1,300 new candidates in three years, about 10% of the global total (Citeline / Norstella, 2025).

- Government backing and landmark deals signal a maturing ecosystem: the 2025 Bio Health Mega Fund of over 224 million euros (Meetings International, 2026) and GSK’s 2 billion pound licensing deal with ABL Bio in April 2025 (BioSpectrum Asia, 2025).

- It is also super-aged, with 20.3% aged 65 or older in 2025, projected to reach 40% by 2050 (Statistics Korea, 2025).

Where Expert Networks Fit in Healthcare PE

Across all markets, a consistent pattern emerges. The variables that determine deal success are rarely captured in macro data.

Examples include:

- How physicians actually adopt new workflows

- Who controls procurement in fragmented hospital systems

- How reimbursement decisions are implemented in practice

- Which local operators have real distribution power

These factors differ not only by country but often by city, hospital type, and payer structure.

As a result, healthcare PE due diligence is increasingly dependent on primary insight from local operators, clinicians, and system participants.

This is where expert access becomes structurally relevant.

Leading healthcare PE investors typically combine:

- macro research (market sizing, policy direction)

- financial modeling (returns, comps, leverage structures)

- local expert input (execution reality)

Expert networks such as GLG, AlphaSights, Guidepoint, and Third Bridge are widely used for this layer of diligence.

In Asia healthcare specifically, this layer becomes more critical due to:

- fragmented provider systems

- uneven regulatory enforcement

- high variability in clinical practice

This is the gap Arches operates in: connecting investors and corporates with physicians, hospital operators, and healthcare executives across the world to validate assumptions that do not appear in datasets.

Healthcare investment in Asia remains one of the most compelling opportunities for global investors. But as competition intensifies, the advantage increasingly comes from understanding the market beyond the numbers.

Beyond the financial models, the firms that win now are the ones asking the right local experts the right questions.

Looking for healthcare expertise in Asia?

Arches connects investors, consulting firms, and corporations with healthcare experts across Asia and global markets, from physicians and hospital executives to healthcare operators and industry specialists.

Frequently Asked Questions

1. How do investors research healthcare markets in Asia?

Most investors combine two layers. Secondary sources such as market reports, filings, and databases give sizing and growth trends. Expert interviews then explain what those numbers miss: physician adoption, procurement behavior, regulation, and local competition. Together they produce stronger, better-informed theses.

2. What are the best expert networks for private equity and healthcare due diligence?

Leading options include GLG, AlphaSights, Guidepoint, Third Bridge, and Arches. Investors usually compare them on industry depth, geographic coverage, compliance standards, and matching speed. For Asia healthcare work, regional expertise and local operating knowledge matter most.

- Follow Arches on LinkedIn for live updates.

- Subscribe to the Arches’ newsletter for monthly insights from our network across Asia and beyond.