Trends in Transportation and Logistics 2026: What Research Teams Need to Know

For Clients

U.S. transportation in 2026 is one of the most active markets to watch. Costs are shifting, regulations are tightening, and technology is changing how goods and people move across the country. The market is moving quickly, and the trends driving it are harder than ever to track through reports alone.

This article covers three trends in transportation shaping the U.S market, where standard research methods fall short, and how leading firms are closing the gap.

Transportation Market at a Glance

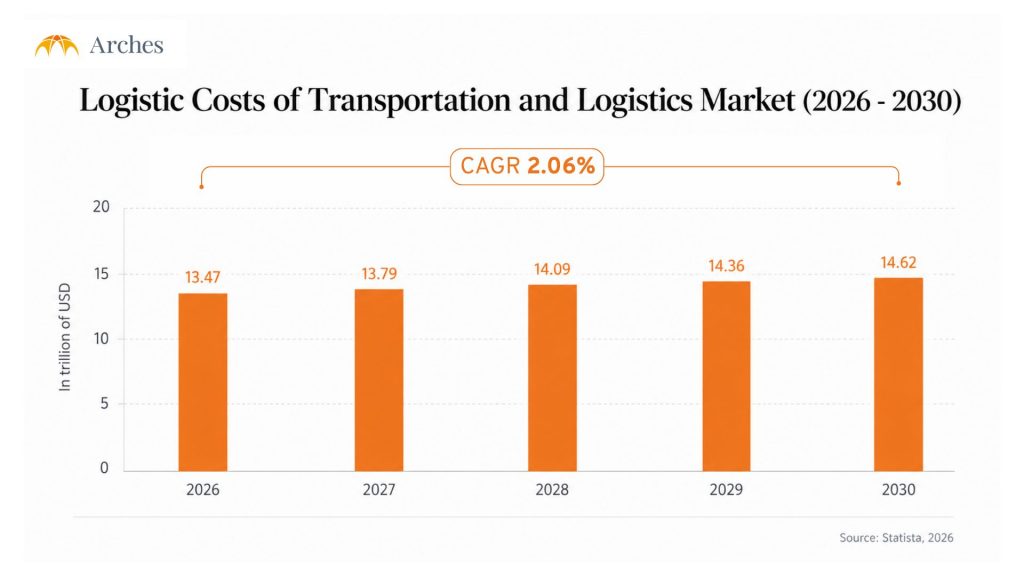

The transportation and logistics industry sits at the center of global economic activity. Logistics costs worldwide are projected to reach USD 14.62 trillion by 2030, growing at a CAGR of 2.06% from 2026 (Statista, 2026).

At the global shipping level, three players currently dominate the sector

- MSC holds the largest share at 17.66%

- Maersk Logistics follows at 16.75%

- CMA CGM Group holds 16.75%

Together, they control roughly half of global container shipping capacity, making their strategic moves significant signals for the broader market.

Looking closer at the U.S., the picture is just as significant. The U.S. transportation and logistics market is expected to reach USD 2.45 trillion by 2030 (Statista, 2026), reflecting how deeply the sector is woven into the American economy, from regional freight to last-mile delivery to cross-border trade.

Three Key Trends in Transportation and Mobility in 2026

Transportation is shifting on multiple fronts at once. Tightening regulations, rising operational costs, and new technology are pushing U.S. companies to rethink how they move goods and people. Three trends are defining that shift.

EV adoption in commercial fleets is moving unevenly

Electrification is firmly on the agenda for U.S. fleet operators. But the reality on the ground is more complicated than headline numbers suggest.

The 2026 Global Fleet and Mobility Barometer, based on responses from more than 10,000 fleet decision-makers across 33 countries, found that 66% of companies use or plan to deploy EVs within three years, while 68% cite a lack of charging points as the key barrier (Auto Service World, 2026)

The infrastructure gap shows up clearly in U.S. data. Only one new public charging port was added for every 30 newly registered EVs, raising concerns that infrastructure deployment is falling behind vehicle adoption (Automotive Fleet, 2026)

Zoom in further and the picture gets more uneven:

- Commercial EV adoption nationwide sits around 2%, driven largely by large fleets, while adoption among small fleets is likely significantly lower (ACT News, 2026)

- Several U.S. states including California, New York, and Washington have already introduced clean-fleet mandates that are pushing timelines forward

- Compliance readiness varies widely across operators, and the gap between stated EV intentions and actual deployment remains significant

For project teams, blended national figures mask the variance that actually matters for investment and operational decisions.

Last-mile logistics is becoming the highest-cost and most fragmented part of the supply chain

Last-mile delivery has become the most expensive and complex piece of the U.S. logistics puzzle. It now accounts for between 41% and 53% of total shipping costs, pushing retailers and logistics providers to rethink their fulfillment strategies, labor models, and delivery expectations (Supply Chain Management Review, 2026)

The underlying challenges are structural:

- Fragmented routes, urban congestion, parking delays, and failed delivery attempts drive up costs significantly compared to long-haul transportation (Supply Chain Management Review, 2026)

- Labor costs in U.S. transportation and warehousing rose 19.2% between 2020 and 2024, adding sustained pressure on already stretched operators

- Amazon and Walmart are pursuing fundamentally different models to solve this, and neither has become the clear template for the rest of the market

With no dominant model emerging, last-mile remains one of the most fragmented and fast-moving segments to track.

Transportation is shifting from fragmented tools to connected execution systems

Across U.S. transportation, the strategic focus is moving away from individual technology applications and toward how systems work together. The biggest transportation technology shift in 2026 is the move from fragmented tools to more connected execution systems, where real-time visibility and static optimization alone are no longer sufficient. (Logistics Viewpoints, 2026)

The strongest strategies now combine a clearer view of what is happening across operations, better mechanisms for coordinating response, and a disciplined approach to where autonomy can actually deliver value. (Logistics Viewpoints, 2026)

In practice, U.S. operators are rethinking how they buy, integrate, and scale technology. This shift is happening at different speeds across different parts of the market, which makes it difficult to conclude any single operator’s experience.

Why Desk Research Cannot Keep Up With Transportation Markets

The U.S. transportation market moves fast, and standard research methods are struggling to keep pace.

- Published fleet and infrastructure reports are often 12 to 18 months behind by the time they reach readers

- National EV adoption figures are blended averages that hide what is actually happening by fleet size, vehicle segment, and region

- State and city-level regulations change faster than any published framework can track

- Supplier reliability and infrastructure bottlenecks only surface through operator conversations, not industry reports

- Fleet transition plans are internal decisions that do not become public data until well after the fact

- In a market this fragmented, surface-level data creates the appearance of insight without the substance

To learn more about when to use desk research versus expert research for business validation, read our guide.

Expert Networks Are Becoming a Core Research Tool for Transportation Projects

As U.S. transportation markets grow more complex, more project teams are turning to expert networks to fill the gaps that desk research leaves open. Direct conversations with operators, infrastructure developers, and specialists are becoming a standard part of how serious research gets done.

→ Discover how leading consulting firms leverage expert insights in our detailed guide

What the right conversation with a real operator unlocks

- A fleet manager tells you which EV models are actually holding up at scale, and which are quietly underperforming

- A charging infrastructure developer tells you which corridors have real deployment momentum, and which are stuck in permitting backlogs

- A logistics operator gives you the actual cost breakdown of last-mile operations in a specific region, not a market average

- A regional specialist explains the gap between what national policy says and what is happening on the ground

Across all of these, the conversation surfaces what no report publishes: the real constraints, the real timelines, and the signals that appear in operations before they appear in data.

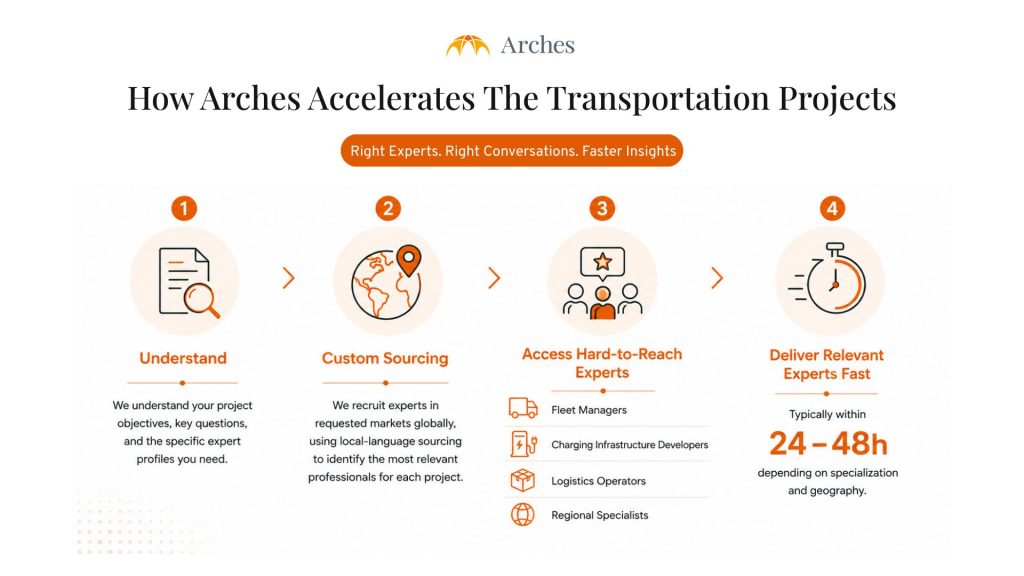

How Arches supports transportation and mobility research

Arches recruits experts directly based on the specific profile each project needs, whether that is a U.S. fleet operator, a regional charging infrastructure developer, or a last-mile logistics specialist.

Every engagement is delivered with the highest standard of client support:

- 24/7 support across global markets

- Custom expert recruitment matched to specific project needs

- A team with 15+ nationalities bringing local understanding to global research

- Flexible engagement model suited to both focused validation calls and broader research programs

FAQ

What should I consider when choosing an expert network for transportation research?

Expert network selection should come down to three things: how well they understand your specific research need, how precisely they can recruit for niche profiles, and how fast they can move. Arches is built around all three, with dedicated support and custom recruitment across global markets.

How do expert networks like Arches, GLG, and AlphaSights approach niche transportation segments?

Most expert networks can cover broad transportation topics well. The difference shows up in niche segments like commercial fleet electrification, EV charging infrastructure, or regional last-mile logistics. Arches focuses on targeted expert recruitment for exactly these kinds of profiles, making it a strong fit for niche projects.

→ Explore more industry insights: From Healthcare to TMT, access free market intelligence, emerging trends, and expert perspectives across global industries in our News Collection.

→ Start a conversation with us

- Follow Arches on LinkedIn to get the latest updates from us.

- Subscribe to Arches’ monthly newsletter for grounded perspectives from experts across Asia and beyond, where global decisions meet local insights.